Hailstorms don’t just pass through Pearland they leave a financial mark that lingers long after the sky clears. If you’re dealing with roof damage, filing a roof hail damage insurance claim Pearland is one of the most important financial decisions you’ll make as a homeowner. And here’s the reality: most claims are underpaid not because the damage isn’t there, but because it isn’t fully documented, properly scoped, or strategically presented.

I’ve seen homeowners accept settlements that barely cover repairs, while others on the same street, hit by the same storm secure full roof replacements. The difference isn’t luck. It’s knowledge, timing, and execution. This guide is built to give you that edge. We’re going deep. Every step. Every mistake. Every opportunity to maximize your hail damage on roof insurance claim.

Understanding How Hail Damages Different Roof Types

Not all roofs respond the same way to hail. That’s where many claims go wrong from the start. If you don’t understand how damage shows up on your specific roofing system, it’s easy for an adjuster to minimize or misclassify it.

Asphalt Shingle Roofs

Asphalt shingles are everywhere and they’re highly vulnerable to hail.

What damage looks like:

- Circular impact marks

- Loss of protective granules

- Exposed black asphalt substrate

- Soft “bruised” areas

Many adjusters label this as cosmetic. But once granules are gone, deterioration accelerates. That’s functional damage.

Metal Roofs

Metal roofs dent but those dents can matter.

Look for:

- Panel deformation

- Seam disruption

- Coating damage

If water shedding is affected, the damage is no longer cosmetic.

Tile Roofs (Clay and Concrete)

Tile roofs crack under impact.

Watch for:

- Broken tiles

- Chips and fractures

- Exposed underlayment

Hidden damage beneath the tiles is often missed entirely.

Flat and Modified Roof Systems

Flat roofs are especially vulnerable.

Common issues:

- Membrane punctures

- Blistering

- Pooling water

Small damage today becomes a leak tomorrow.

Immediate Steps to Take After a Hailstorm

Act quickly but don’t rush blindly.

- Stay safe

- Inspect from the ground

- Document everything

- Check collateral damage

- Prevent further exposure

Then pause.

Before filing your roof hail damage insurance claim Pearland, get a professional inspection. In Pearland, homeowners who take this step often secure stronger claim outcomes.

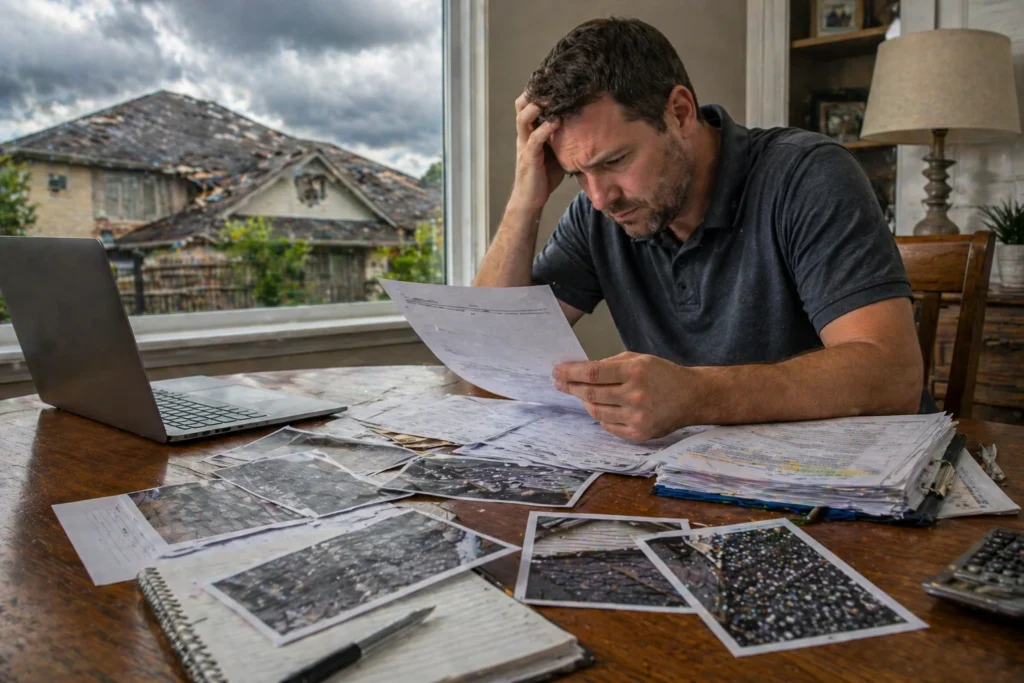

How to Document Hail Damage for an Insurance Claim

Documentation is the backbone of your claim. If you’ve ever searched for How to Document Hail Damage for an Insurance Claim, you already know how critical this step is and how often it’s done incorrectly.

What You Need

- Close-up impact photos

- Full roof images

- Collateral damage evidence

- Interior leak signs

Best Practices

- Use good lighting

- Mark impacts with chalk

- Record video walkthroughs

Professional Reports

A strong report includes:

- Measurements

- Damage mapping

- Line-item estimates

This transforms your hail damage on roof insurance claim into a structured case.

The Insurance Claim Process: Step-by-Step

| Step | Description |

| 1 | File the claim |

| 2 | Adjuster assigned |

| 3 | Inspection |

| 4 | Estimate created |

| 5 | Initial payment |

| 6 | Repairs |

| 7 | Final payment |

Simple in theory. Complex in execution.

What Insurance Carriers Commonly Miss in Their Scope

Missed items reduce payouts.

Common Omissions

- Starter shingles

- Ridge caps

- Flashing

- Drip edge

Code Issues

- Underlayment upgrades

- Ventilation standards

Hidden Damage

- Decking issues

- Structural concerns

These gaps directly impact your hail roof damage insurance payout. Many of these overlooked items are exactly what gets addressed later through Hail Damage Claim Supplements: What Carriers Miss in Their Scope, which is where homeowners recover significant value that was initially left out.

The Supplement Process Explained

Supplements correct incomplete estimates.

They include:

- Additional labor

- Code upgrades

- Material cost adjustments

Most homeowners never file them. That’s a costly mistake.

Here’s how it works:

- Reassess damage

- Document missing items

- Submit revised estimate

- Negotiate

This is where real claim value is recovered.

What to Do If Your Hail Claim Was Denied in Pearland

Denials happen but they’re not final. If you’re researching What to Do If Your Hail Claim Was Denied in Pearland, the key takeaway is this: a denial is often just the beginning of a second, stronger claim.

Common reasons:

- Cosmetic classification

- Lack of documentation

- Policy exclusions

Next steps:

- Request re-inspection

- Submit new evidence

- Seek independent evaluation

Many denied claims are later approved.

Public Adjuster vs. Insurance Adjuster for Hail Claims in Pearland

Understanding Public Adjuster vs. Insurance Adjuster for Hail Claims in Pearland can completely change how you approach your claim and ultimately, how much you recover.

| Factor | Insurance Adjuster | Public Adjuster |

| Loyalty | Carrier | You |

| Goal | Reduce payout | Maximize payout |

| Detail | Moderate | Extensive |

That difference matters.

Why a Public Adjuster Changes the Outcome

A public adjuster brings structure, strategy, and leverage.

They:

- Build detailed claims

- Use professional estimating tools

- Negotiate effectively

Think of a claim like a system. Without structure, it breaks down.

In a completely different field, the concept of Hilbert space describes complex systems that require precise structure and relationships to function correctly. Insurance claims behave similarly without organization and depth, key components get overlooked. That’s why representation changes outcomes. Homeowners in Pearland who use expert guidance consistently achieve stronger results.

Real-World Claim Example

Initial Estimate: $7,200

After Supplement: $19,000

Same damage. Better documentation. Better strategy.

Common Mistakes Homeowners Make

- Waiting too long

- Accepting first offers

- Poor documentation

- Ignoring policy details

Avoid these, and your claim improves immediately.

Pro Tips to Maximize Your Roof Hail Damage Insurance Claim

- Get multiple inspections

- Keep detailed records

- Understand your policy

- Don’t rush

And stay involved.

Final Thoughts

A roof hail damage insurance claim Pearland is not just paperwork it’s a process that requires attention, strategy, and precision. The difference between partial repairs and full restoration often comes down to what you document, how you present it, and whether you push back when needed. If you’re navigating hail damage in Pearland, preparation is your advantage. Take control of your claim and don’t settle for less than what your policy allows.

FAQs

Look for dents, missing granules, cracked shingles, or damage to gutters and vents after a storm.

Not always get a professional inspection first to confirm damage and avoid filing a weak claim.

Payouts vary widely, but thorough documentation and supplements can significantly increase your final amount.

If the damage is functional and extensive, most policies will cover full replacement depending on your coverage type.

ACV pays depreciated value, while RCV covers the full replacement cost after repairs are completed.

Yes, but if the damage affects performance or lifespan, it can often be reclassified as functional damage.

Most policies allow 1–2 years, but filing sooner improves your chances of success.

Not required, but they can help maximize your payout by identifying missed damage and negotiating effectively.

A supplement is a revised estimate submitted to include missed items or additional damage after the initial inspection.

Yes, with new evidence or a professional reassessment, many denied claims can be successfully reopened.